3 Actuaries and Actuarial Thinking

3.1 A Brief History Lesson

The quantification of risk has been in existence for thousands of years. The Code of Hammurabi from 1750 BC made early attempts to calculate arrangements for bottomry. This is where the master of a vessel borrows money upon the bottom (or keel) of it, so as to forfeit the ship itself to the creditor, if the money with interest is not paid at the time appointed at the ship’s safe return.

Early Origins: Pre-17th Century Evidence of rudimentary actuarial practices appears in ancient Egypt, Greece, and Rome, where societies pooled resources to support widows and orphans, as well as to cover burial expenses. These early societies recognized risk-sharing as essential, though the mathematical understanding was limited. In the Middle Ages, guilds formed in Europe that provided mutual support to members in the form of pensions and sickness benefits. While these weren’t actuarial systems per se, they represented early forms of mutual aid systems that would later be refined mathematically.

Development of Probability and Mortality Tables: 17th Century The modern mathematical underpinnings of actuarial science began with the development of probability theory. Mathematicians like Blaise Pascal and Pierre de Fermat in France worked on problems of chance, paving the way for calculating risk. In the 1660s, John Graunt, a London haberdasher, and demographer, created one of the first mortality tables by analyzing death records. Edmond Halley (known for Halley’s Comet) later refined these tables by creating the first actuarial table that allowed for the calculation of life annuities based on age.

Birth of Life Insurance and Formal Actuarial Practice: 18th Century The Amicable Society for a Perpetual Assurance Office, established in London in 1706, is often considered the first life insurance company. However, it was not based on actuarial principles and struggled with sustainability. In the mid-1700s, James Dodson, a mathematician, noticed the deficiencies of the Amicable Society’s approach. Dodson advocated for fairer premiums based on age, which led to the founding of the Equitable Life Assurance Society in 1762, the first life insurance company based on actuarial principles. The society employed the first actuary, William Morgan, in 1775, who is often called the “father of actuarial science.”

Formalization of Actuarial Science: 19th and 20th Centuries Actuarial science continued to gain momentum in the 19th century, especially in the UK, where actuaries were establishing rigorous standards. The Institute of Actuaries was formed in London in 1848, followed by the Faculty of Actuaries in Scotland in 1856. Actuarial work expanded beyond life insurance to include pensions and health insurance. The British government commissioned actuaries to help develop pension plans and other social insurance schemes, further professionalizing the field. Actuarial practices spread internationally, especially in North America, where the Actuarial Society of America (now part of the Society of Actuaries) was founded in 1889. Actuarial societies also emerged in Australia, Canada, and South Africa.

With the computers becoming more available and accessible, actuaries could handle more complex calculations, incorporating techniques like multivariate statistics, survival analysis, and stochastic processes. Actuarial science expanded into financial mathematics, especially in the areas of risk theory, asset-liability management, and portfolio theory. Actuaries began to contribute to investment analysis, pricing of financial derivatives, and enterprise risk management. Governments in the early 20th century increasingly relied on actuaries to design social security systems, health insurance plans, and public pension schemes, reinforcing actuarial science’s role in public policy.

- Contemporary Era: Late 20th Century to Present Actuaries have expanded into non-traditional fields, including data science, environmental risk, predictive analytics and PA. With the rise of big data, actuaries now apply machine learning algorithms and artificial intelligence to refine risk predictions. Since the 1990s, actuaries have increasingly been involved in Enterprise Risk Management (ERM), providing companies with a holistic approach to managing all aspects of risk. Actuarial societies now exist worldwide, and many follow global standards set by the International Actuarial Association (IAA). Actuarial education has also become more standardized, with rigorous exams covering probability, financial mathematics, and actuarial modeling.

3.2 How do Actuaries Solve Problems?

Actuaries possess a unique blend of technical, analytical, and business-oriented skills. Their expertise allows them to assess and manage financial risks, primarily in insurance, finance, and pensions. Actuaries have been working with vast amounts of data and complex algorithms before computers even existed. As data has become more accessible and computational power increased substantially, actuaries have found themselves branching out to other fields that could benefit from their skills including management consulting, marketing, finance and now PA!

3.2.1 The Actuarial Control Cycle

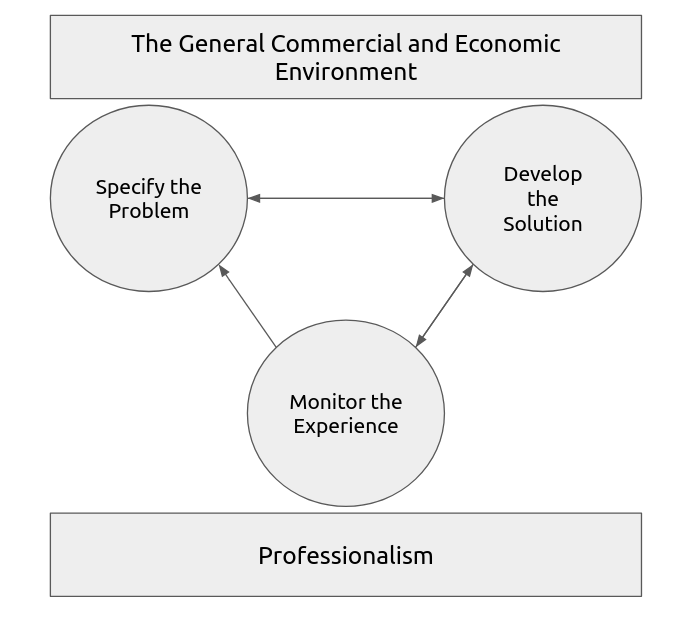

The Actuarial Control Cycle (ACC) is the core framework used by actuaries to systematically approach problem-solving, particularly in areas involving financial risk and uncertainty. It is a structured, iterative process that helps deliver reliable and informed outcomes, while also managing and mitigating risks. The cycle consists of three main stages:

-

Specifying the Problem

- The first step is to clearly define the business problem that needs to be addressed. This might involve managing financial risk, pricing products, evaluating investment strategies, etc

- Key Activities:

- Identify the client’s objectives.

- Set out the problem from each stakeholder’s view

- Assess the risks for each stakeholder

- Consider mitigation strategies for each risk

- Analyse risk transferring options betweek stakeholders

- Understand the scope of the problem.

- Gather relevant information (financial, demographic, or market-related).

- Clarify the constraints, such as regulatory or financial limitations.

- Questions to Ask:

- How will the results be reported and to whom?

- What will the implications of the results be and for whom?

- How will implementation of the results of proposals be monitored?

- What can be learnt from the actual outcomes compared with those expected?

- What resources are required?

- Is the timescale for task completion reasonable?

- What expertise is required?

- Will the advice be used for executive action or is it purely advisory?

- Who owns the problem

- What are the questions that need answering?

- Can it be broken down into smaller problems?

- Will answers be relevant in finding an optimal solution to the problem?

-

Developing the Solution

- Once the problem is defined, actuaries develop a solution, typically using mathematical models, statistical techniques, and financial theories. This stage involves analysing data, making assumptions, and building models to project future outcomes.

- Key activities:

- Examine major models in use

- Gather and analyse the data needed to model the problem

- Select or construct appropriate models

- Consider assumptions

- Understand the sensitivity of assumptions

- Interpret the results of the model

- Consider the implications of the model to the problem and the stakeholders

- Determine a proposed soluion to the problem

- Consider alternatives and their effects

- Formalise a proposal

- Modelling and Assumptions: Develop models and make key assumptions.

- Scenario Testing: Test various scenarios to understand how different factors impact the results.

- Solution Design: Develop strategies or solutions based on the models.

-

Monitoring the Experience

- After implementing the solution, it is critical to continuously monitor the results to ensure that the original assumptions and models are still valid, and that the desired outcomes are being achieved. The environment (e.g., economic, demographic, or market conditions) can change, so adjustments might be needed.

- Key activities:

- Performance Monitoring: Track actual outcomes and compare them with the expected results.

- Make sure the solution is dynamic and that it reflects current experience

- Periodically analysing actual experience against expected

- Identify causes of departure and if they are once off or recurring

- Feedback into specifying the problem and “developing the solution” stages

- update assumptions as to future experience

- monitor any adverse trends in experience so as to take corrective actions

- provide management information

- Experience Analysis: Analyse deviations between actual and expected outcomes to identify trends, anomalies, or risks.

- Feedback and Review: Use the results to review the assumptions and models. If the outcomes differ significantly from what was projected, the solution may need to be adjusted. These steps are connected by feedback loops, allowing actuaries to continually refine their models and strategies based on new data and evolving conditions.

The ACC ensures that actuarial decisions are grounded in rigorous analysis, incorporate up-to-date assumptions, and adhere to regulatory standards. By following this cycle, actuaries ensure their solutions are dynamic and responsive to changes, offering businesses robust solutions to their financial, risk and analytical problems.

Many of you may notice the similarity between this and various data science or analytical problem solving frameworks. Where I find this differs is in 2 aspects not commonly considered, namely, professionalism and economic considerations.

-

Professionalism

- Throughout the ACC, actuaries must adhere to professional standards, ethical guidelines, and legal or regulatory requirements. This includes ensuring transparency, objectivity, and accountability in the work they perform.

- Key Activities:

- Comply with ethical standards of practice.

- Ensure adherence to relevant laws and regulations.

- Communicate clearly and effectively with stakeholders, including clients, regulators, and the public.

-

Being aware of the general commercial and economic environment

- Key Considerations: -External environment -Stakeholders -Providers of benefits -Economic Influences -Regulation -Insurance products -Asset Classes

Figure 3.1: The Actuarial Control Cycle

What makes this actuarial is:

- The estimation of financial impacts of uncertain future events

- Considering a long term horizon and making decisions in light of likely future outcomes

- Consideration of stakeholders, legislation, tax and competition

- Use of assumptions based on appropriate historical experience

- Use of models and interpretation of the results to develop strategies

- Monitoring and periodically analysing the emerging experience to update models built

Finally, it is also important to consider the concepts of proportionality and materiality in one’s work. Work performed must be proportionate to the scope of the decision/assignment it relates to and to the benefit clients expect to obtain from the work. Work is material if it could influence the decisions to be taken by users of the related information. Assessing materiality is a matter of reasonable judgement which requires consideration of the clients and the context in which the work is performed and reported.

By employing the techniques explained here and thinking about PA problems from with risks and financial impacts in mind, you can truly be a more strategic contributor to your company and aid in improving the experience of your fellow employees as well as to the bottom line.

3.3 Does it Work?

I’ve used the ACC to save my company millions of dollars. During a project appraisal, the HR team put together and assessment of a vendor. Upon reviewing this, I thought more work was needed and applied the ACC and actuarial project appraisal techniques (chapter 8) to better assess the purchase. This took much time and annoyed some senior colleagues, but, upon completion, I had all the numbers backing up my assessment and enough data to prove that the value that the vendor claimed could be derived was very far from what we could actually achieve. Now, the decision moved from being a financial and advancement positive “no brainer” to being quite a financial black hole in exchange for advancement of processes. This helped the key decision makers understand what was being bought and also removed any expectations of positive financial returns from the purchase. By having this, it made sure that HR was not going to be pressured to force value out of something that couldn’t deliver such benefits. The company eventually didn’t buy the software as none of the financial metrics could make up for the other positives. Had the company blindly bought the software, it is highly likely that the subscription would have been subsequently cancelled and many leaders losing credibility for bad decision making when their financial expectations did not materialise.